Although the topic is not new, it seems that there are always new things to say about investor-State arbitration when looking at the amount of articles and documents issued and published almost on a daily basis by the EU Commission and Parliament, national governments and parliaments but also academics, practitioners, the media, blogs, etc. This very technical topic which used to be discussed only among specialists is now clearly involving the general public, media, newspapers and politicians and it can now be said that the man on the street is becoming familiar with notions such as ISDS, appellate mechanisms, fair and equitable treatment, full protection and security, etc.

I. Investor-State arbitration: a Historical Perspective

Investor-State arbitration is not new and disputes between States and investors relating to the use of the States’ natural resources go back to the first half of the 20th century and were mainly ad hoc arbitrations. Interesting, in these early arbitrations, it was already clear that the disputes should remain between the investor and the State and not escalate between the host State and the State of the nationality of the investor, and this became the fundamental philosophy behind the foundation of the ICSID. It was considered appropriate to place these disputes in an institutional context to administer them on the basis of uniform procedural rules rather than conducting arbitrations on an ad hoc basis.

The first decades of existence of ICSID did not attract much attention, very few cases were registered and it was mainly a topic of interest for specialized academics and public international law lawyers rather than practitioners and investors. The huge potential of this mechanism was discovered in the 90s when it was understood that it could be used in conjunction with the network of bilateral investment treaties which lay down substantive and jurisdictional rules for the protection of foreign investors. This resulted in the success of investor-State arbitration with two recent developments which are worth mentioning. First, in the recent years, we have heard widespread criticism by States of certain features of the ICSID system and this led to some disputes which were almost exclusively brought before ICSID to being brought before other institutional fora such as the PCA, the Stockholm Institute or the ICC. Second, the discussions and negotiations about the free trade and investment protection agreements between the EU and some of its principal trade partners are one of the underlying reasons for the public’s interest in the topic and result from the EU’s acquisition of exclusive external powers since the Lisbon Treaty.

In particular, the most advanced negotiations concern the Comprehensive Economic and Trade Agreement with Canada (CETA), the EU-Singapore Free Trade Agreement and the Transatlantic Trade and Investment Partnership with the United States (T-TIP). When negotiations began a few years ago, it was immediately envisaged that the new Agreements would reproduce the scheme of BITs and MITs and would also provide for investor-State arbitration. The transparency in these negotiations triggered the general interest and, as a consequence, widespread criticism of the traditional system of investor-State protection. With respect to the substantive standards of protection, the most extreme positions State that the agreements are a threat to democracy and sovereignty of States (in particular to their right to regulate sensitive matters). With respect to the dispute resolution system, the criticisms concern the threat to sovereignty which results from empowering private judges. These criticisms have obtained certain results as the current draft texts of the CETA, the EU-Singapore Agreements and the T-TIP contain significant departures from the usual provisions of investment treaties. The question is therefore whether we are going towards a revision of the traditional investor-State dispute resolution system or a complete abandonment of the system.

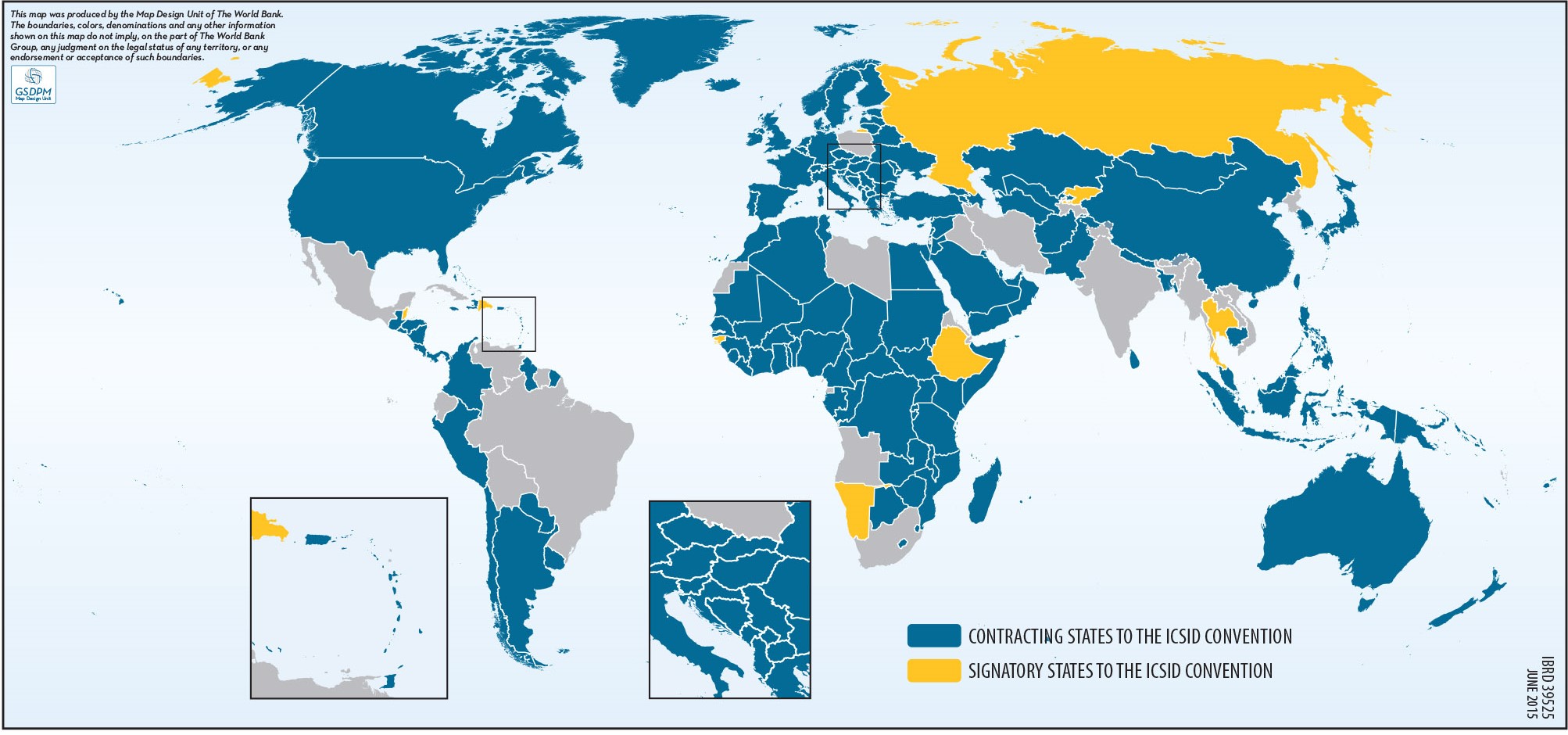

Investor-State Disputes: States that Have Ratified the ICSID Convention

II. The EU’s Investment Policy and the New Agreements

Further to the Lisbon Treaty, the EU developed an investment policy through several steps. The first step was the Commission’s Communication of 7 July 2010 entitled “Towards a comprehensive European Union international investment policy” in which it recognized the importance of investor protection and a system of “guarantees from third countries on the conditions of investment [which] should come in the form of binding commitments under international law”. This indeed requires going beyond the BIT system. The Communication also highlighted the importance of the enforcement of agreements and, in addition to State to State dispute settlement mechanisms, the Communication also referred to the need for investor-State dispute settlement. In particular, the Communication States that it is “such an established feature of investment agreements that its absence would in fact discourage investors and make a host economy less attractive than others”. The main challenges of the Communication relate to ensuring the transparency of these mechanisms and the consistency and predictability of the outcome, and it also refers to the need for quasi-permanent arbitrators and/or appellate mechanisms.

In response to the Commission’s Communication, the Parliament issued a Resolution on the future of European investments on 6 April 2011 and highlighted the need for the Parliament to be involved in the shaping of the investment policy. The Parliament expressed “its deep concern regarding the level of discretion of international arbitrators to make a broad interpretation of investor protection clauses, thereby leading to the ruling out of legitimate public regulations”. Specifically, on dispute resolution mechanisms, the Parliament agreed with the Commission that “in addition to State-to-State dispute settlement procedures, investor-State procedures must also be applicable in order to secure comprehensive investment protection”. The Parliament also emphasizes the need for “greater transparency, the opportunity for parties to appeal, the obligation to exhaust local judicial remedies where they are reliable enough to guarantee due process, the possibility to use amicus curiae briefs and the obligation to select one single place of investor-State arbitration”. Although there are differences among the EU institutions, they acknowledge the need for investor-State settlement mechanisms in the treaties to be negotiated and agree that they must be adapted to satisfy new concerns. More recently, a regulation of 23 July 2014 confirmed that ISDS would remain part of the new regimes and instruments.

The scope of the Agreements with Singapore and Canada is meant to be a lot broader than foreign investments, the negotiations have ended and the texts are now subject to review and ratification. The two texts are a good indicator of where the EU stands with respect to investment policy. It is clear from the texts that the drafters have tried to take into account some of the criticism as they depart significantly from the usual provisions contained in BITs. For example, the treaties contain provisions such as the following:

- The CETA provides that “an investor may not submit a claim to arbitration under this Section where the investment has been made through fraudulent misrepresentation, concealment, corruption, or conduct amounting to an abuse of process” which reflects famous ICSID cases, and provides that ISDS “shall apply to the restructuring of debt issued by a Party in accordance with Annex X (Public Debt).”

- Both Agreements provide that claims can be brought under the ICSID Convention, the ICSID Additional Facility, the UNCITRAL rules or other rules agreed upon between the Parties.

- Both Agreements adopt the Commission’s reference to quasi permanent arbitrators and refer to the possibility of the arbitrators being appointed by the Secretary General of ISCID from a list of 15 individuals with suitable expertise in international law.

- With respect to the interpretation of the Treaties, the drafters attempted to enhance consistency by referring to a Committee which has the power to adopt interpretations of the agreement which are binding on the tribunals, even during ongoing cases.

- Both Treaties grant the tribunals the power to suspend the proceedings on the merits and decide on a preliminary question or objection.

- The Treaties also contain new provisions about the non-disputing party, the EU (rather than the member States) or Singapore, which must be informed of the dispute and provided with all relevant documents and information regarding the dispute and the proceedings. The non-disputing party can also participate in the proceedings, if invited by the tribunal, by making oral or written submission or attending hearings.

- With respect to the enforcement of awards, the ICSID system is abandoned and the Treaties refer to national procedural law.

- The Agreements do not refer to appellate mechanisms but the contracting parties reserve the right to consult on the creation of such mechanism.

Originally, the drafts of the Canada and Singapore Treaties served as a basis for the negotiations of the Transatlantic Trade and Investment Partnership. In March 2014, in response to public concerns, the EU Commission launched a public survey and the results revealed a widespread opposition to the ISDS mechanism which was perceived as a threat to democracy and public finances and policies, and considered unnecessary between the EU and the US in light of the strengths of the parties’ respective judicial systems. As a result of this movement, the EU institutions have become even more hesitant about the inclusion of investor-State settlement mechanisms in the Transatlantic Trade and Investment Partnership.

A concept paper published in May 2015 by the EU Commission reflects this criticism and takes an approach very different from the traditional BITs as it refers to a multilateral system for the settlement of investor-State disputes and the institution of a permanent dispute court and an appellate mechanism. The EU Parliament recommended that the Commission uses the concept paper as a basis for future negotiations and suggested the establishment of a public international investment court.

The draft text of the Transatlantic Trade and Investment Partnership was published very recently by the EU Commission and is an internal document which is not used to negotiate with the US but to consult with member States and the Parliament. A reading guide summarizes the content of the draft and indicates that, in parallel to Transatlantic Trade and Investment Partnership negotiations, the Commission will start working on the establishment of a permanent investment court which, overtime, would replace all investment dispute mechanisms provided in EU Agreements and EU member States’ agreements with third countries and in trade and investment treaties concluded between third countries. The text proposes court systems, rather than investor-State arbitral mechanisms, composed of a tribunal of first instance with 15 publically appointed judges and an appeal tribunal with 6 publically appointed judges. The 15 judges would be appointed jointly by the EU and the US (5 EU nationals, 5 US nationals and 5 nationals of third countries), disputes would be allocated randomly so the disputing parties would have no influence on the selection of the three judges who would hear the case, and the same would apply to the judges of the appeal court. In order to avoid the “double hat”, judges would be prevented from acting as counsels on cases.

The system is described in the guide as a new era in the settlement of investment disputes and it appears that the opposition to an arbitral ISDS has prevailed. Whether this new system will be accepted by member States and the US remains to be seen and it is unclear to what extent these most recent approaches will have an impact on already negotiated texts such as the Agreements with Canada and Singapore.

Advocates for the current ISDS system have been rather silent; practitioners and institutions have only recently started to engage in a public debate and expressed the view that, although there is room for improvement, much of the criticism of the current ISDS system is based on improper knowledge.

The ISDS system has been a matter of great controversy because of the involvement of the EU and its institutions which are concerned with safeguarding the predominance of the EU laws, and also because most of the existing BITs were conceived to protect investors from developed countries against measures taken by less developed countries, which is a situation that has now evolved because of a general change in economic and political conditions (the most developed States are now sometimes respondents in the disputes). The fact that the reliability of the legal systems of the contracting parties (the EU and the US, Singapore or Canada) is similar also contributes to the debate. However, it can be said that the need for an effective arbitral mechanism to protect investment does not only depend on the reliability of the judicial system of the host State but also on the investor’s preference to litigate before an international neutral forum rather than a local court.

III. Possible Outcomes of the Debates Concerning the ISDS Mechanisms

The debate is indeed very politicized and insufficiently informed. The data reported relating to the success of investor-State arbitrations are very often wrong and focus on certain mediatized cases while failing to understand fully their implications. There are several possible outcomes of the current debate:

- The first possible outcome is an outright abandonment of the current ISDS system with the consequence that jurisdiction would return to host States’ courts. This would be a very unwelcomed outcome as it would decrease the level of protection of the investor and constitute a disincentive to foreign investments. The level of competence and experience of local courts in international investment law is also a concern.

- The second possible outcome is the creation of a permanent investment court which would of course have a much less negative impact; this idea is not new. The prospects of creating such mechanism within a short timeframe are quite unlikely. It is doubtful that it would avoid the risk of unpredictability of the outcome of the cases and this system would be a lot less flexible with respect to selecting arbitrators.

- The third possible outcome is maintaining the current arbitral system while introducing substantial changes to address the States’ concerns. This is strongly reflected in the texts of the Canada and Singapore Treaties and a number of issues should be addressed. First, the selection of quasi permanent arbitrators would lead to an imbalanced pool of arbitrators which the investors would not necessarily trust. Second, in relation to the appellate mechanism meant to ensure consistency and allow the corrections of errors, it is evident that divergences in jurisprudence and a certain degree of unpredictability are typical of any dispute resolution system. Third, with respect to the transparency which has now become an inner characteristic of investor-State arbitration, more could be done to respond to the growing demand for transparency without posing any threat to the current functioning of the ISDS system, for example through the use of transparency rules (UNCITRAL).

To conclude, although the current BIT system is not perfect, it has proven largely adequate to achieve its mains goals which are to ensure that foreign investments are protected by dispute settlement mechanisms which investors can trust, and encourage direct investment. Criticisms largely miss the point in that they focus on the dispute settlement system rather than the substantive rules and standards and their applications, which are a lot more complex. Rather than criticizing the arbitrators for what they might to in the future, the public should focus more on the substantive standards as there is of course a lot of room for improvement. Regardless of the merits of the criticism of the investor-State arbitration system, there is a serious risk of spillover to commercial arbitrations.

Keynote speech by Andrea Carlevaris, INVESTMENT ARBITRATION IN PRACTICE: A VIEW FROM THE INSIDE, Conference of 26 September 2015, Geneva (YAF, ICC, CISD)